ESG in '23

ESG in '23

A discussion of trends we’ve observed over the past year and ESG considerations for different stakeholder groups going into 2023.

The capital markets and regulatory landscapes have evolved dramatically over the last year as a result of changing consumer preferences related to sustainability and climate action. In prior posts, we talked about Climate Regulations Under the Biden Administration, the Nexus Between Shareholder Activism and Sustainability, the Greening of the Financial Sector, and the environmental and social implications of cryptocurrency and blockchain technology.

Today’s installation of “The Green Tea” will summarize trends we’ve observed over the past year and break down ESG considerations for different stakeholder groups going into 2023.

Key Takeaways

For Board Members

Prepare for a new wave of ESG-related proxy voting

Take ownership of ESG issues

For Executives

Expect ESG to influence your compensation

Set targets… and then show your progress towards these targets

For Investor Relations Professionals

Plan to integrate proactive outreach and governance/ESG meetings into the 2023 IR calendar

Expect a little frustration when engaging with ESG raters and filling out surveys

Prioritize engaging with a broader group of stakeholders

For Investors

Prepare for mandated climate-related disclosures

Expect a global framework to materialize paving the way for more consistent disclosure

The SEC & EU FCA will continue to identify greenwashing, so prepare to back ESG-related claims with empirical data

Develop a plan for engaging with LPs on ESG topics

For Bankers

Expect ESG to impact M&A

Plan for changing access to capital

Watch out for the rise in sustainability-linked debt issuances

Understand the ways that ESG will continue to influence IPOs

For Interns / Students

Build your foundation in school by choosing a related major

Work on your people skills and professionalism through informational interviews

Get involved - either through an internship, volunteer work, or student organizations

For the Board Member

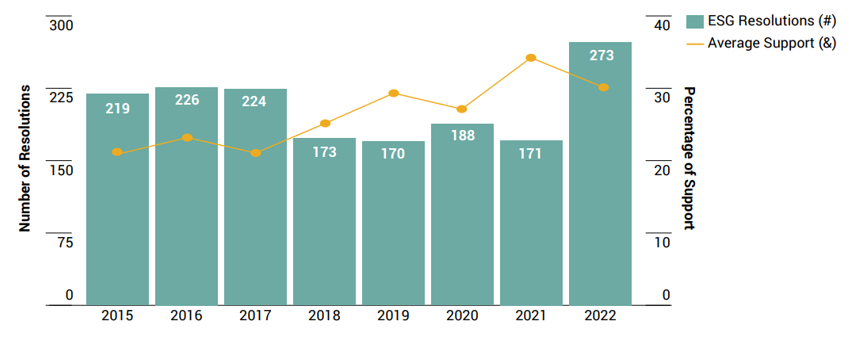

Prepare for a new wave of ESG-related proxy voting: ESG factors have become a key consideration going into proxy season. Over the last several years, we’ve seen a rise both in the number of ESG-related shareholder proposals and the average support for these proposals (Sustainalytics). We’ve also seen a rise in the number of directors being voted against on the basis of inadequate oversight of ESG-related issues. These trends indicate that directors need to understand the issues that stakeholders care most about and be fluent in the ESG issues facing a company.

Take ownership of ESG issues: To expand on the prior topic - stakeholders expect board members to have oversight of a company’s management of ESG issues. Increasingly, we are seeing companies tasking specific committees with this oversight. A 2021 study by NNIP shows that 62% of companies in the U.S. have dedicated responsibility for ESG oversight at either a standalone or combined committee level. Interestingly, stand-alone committees are most prevalent in the energy sector (44%), followed by materials (37%). According to this study, companies with stand-alone ESG committees do tend to have stronger ESG performance, reflected by higher ESG scores.

For the Executive

Expect ESG to influence your compensation: Typically, executive compensation is linked to financial performance. However, over the last several years, we’ve seen companies starting to link executive compensation to non-financial factors, including performance on ESG topics. Now, executive compensation at 73% of S&P 500 companies is now tied to ESG performance (Fortune). However, ESG performance can refer to a wide swath of topics. Most commonly, we see companies tying executive compensation to their health & safety, diversity & inclusion, and carbon emissions goals. There are a couple of different approaches for factoring ESG performance into compensation. Companies can incorporate quantitative targets and gauge whether or not those targets were hit, including ESG factors in a broader qualitative assessment of strategic achievements, or even use ESG factors as a final modifier, to adjust the final payout under the incentive plan. For more information about how companies are integrating ESG into their incentive plans, here’s a great article from Forbes.

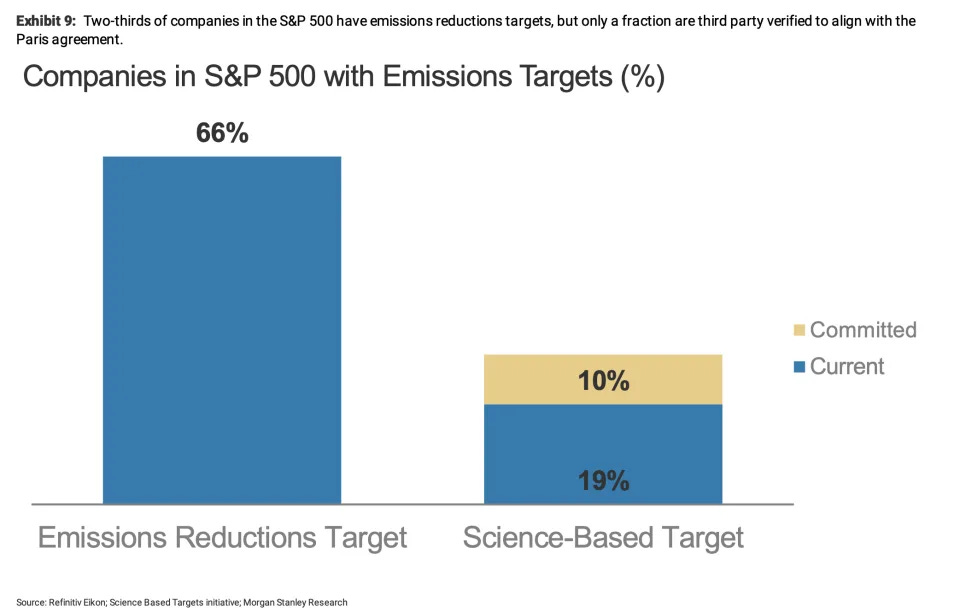

Set targets… and then show your progress towards these targets: In 2021, over 67% of S&P 500 companies had set targets to reduce their greenhouse gas emissions according to a note by Morgan Stanley (Yahoo! Finance). At that time, mentions of "net zero" and other sustainability themes had been on the rise at corporate events, but only 29% of S&P 500 companies have implemented or plan on implementing science-based targets. While we don’t have updated figures from Morgan Stanley, it’s fair to assume these percentages have all increased due to increasing investor pressure and the SEC’s proposed rule on climate-related disclosures. However, over the last year, we’ve seen shifting investor sentiment towards long-term goals. Where “net zero” goals were once seen as best in class, investors now expect companies to set achievable short and medium-term targets and disclose quantitative metrics showcasing their progress towards these targets.

For the Investor Relations Professional

Plan to integrate proactive outreach and governance/ESG meetings into the 2023 IR calendar: In 2018, MiFID II shook up how investor relations programs are run. Decreasing sell-side coverage (especially in the mid and small-cap space) meant that investor relations officers and teams needed to be proactive, sometimes even conducting independent outreach to the buy side. Through 2019 and 2020, we saw asset managers building their own corporate access desks and portfolio managers gladly meeting with the issuers who reached out to them directly. Turnover on the buy side, hiring of stewardship and ESG research teams, and the renewed ability to travel make 2023 a critical year for issuers to conduct regular, proactive outreach to the buy side. It is vital to educate these new faces on your company’s ESG story and explain how you are differentiated from your peers. While this outreach can certainly take the form of 1x1s, increasingly we are seeing corporates conducting governance or ESG roadshows, focused solely on meeting with stewardship contacts.

Expect a little frustration when engaging with ESG raters and filling out surveys: For any investor relations teams who have been tasked with filling out Corporate Sustainability Assessment from S&P, correcting data in MSCI’s issuer platform, or completing inbound ESG due diligence surveys from investors - it won’t be a surprise that this is repetitive, often frustrating work. While it may seem unrewarding at the time, filling out these surveys can pay dividends in terms of increasing access to investor capital. For instance, an upgrade in letter grade from MSCI can result in new access to billions of dollars of ESG ETFs and index funds. Even if you think you have it made because your company has a “AAA” from MSCI or an “A” from CDP - it is important not to rest on your laurels. Raters like MSCI and EcoVadis have announced updates to their scoring methodology going into next year - they are raising the bar to “keep up with increasingly more sophisticated disclosure from corporates” (we are paraphrasing here).

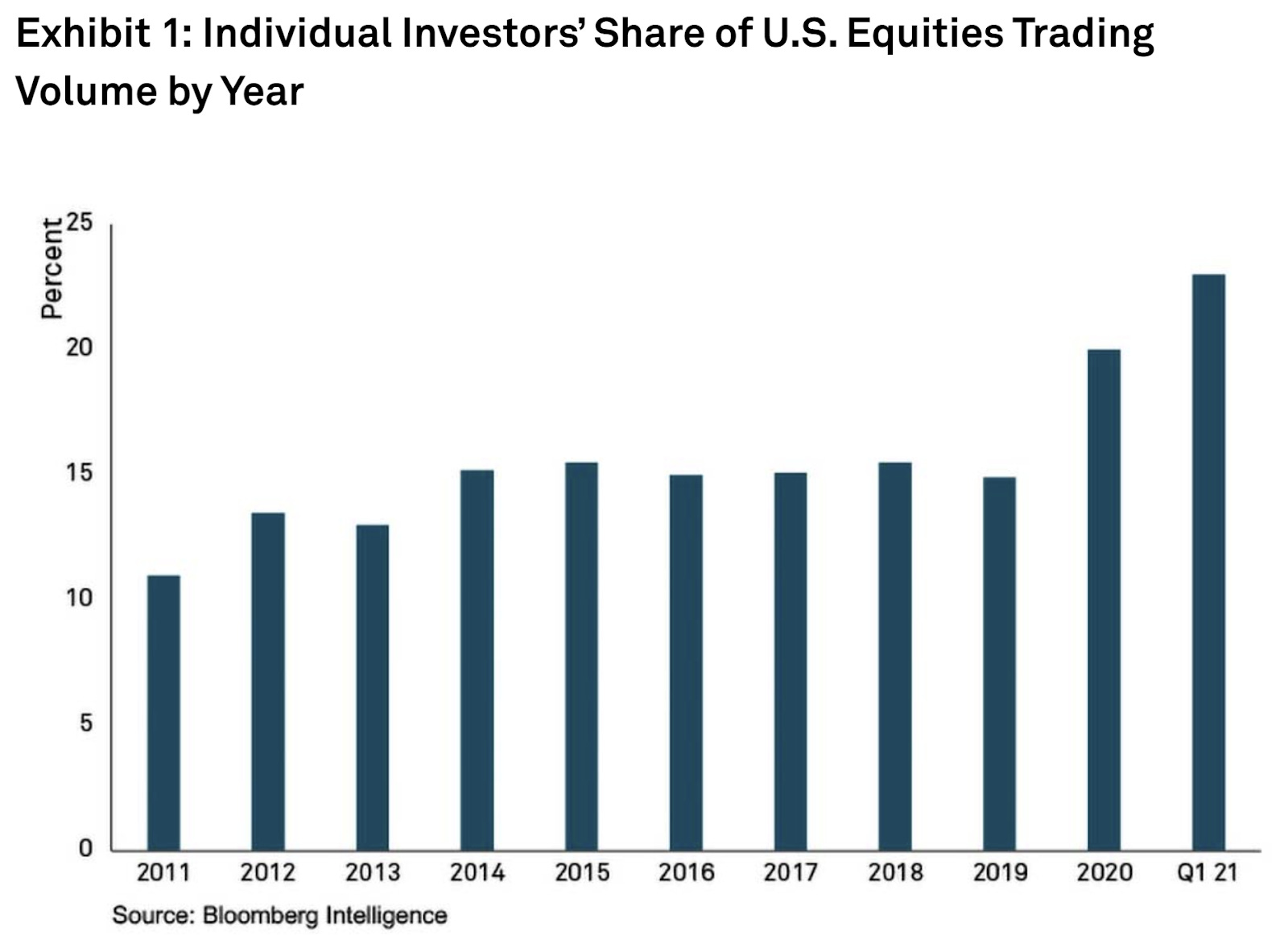

Prioritize engaging with a broader group of stakeholders: On top of traditional portfolio managers and analysts, investor relations professionals have a growing group of stakeholders to engage with. According to BNY Mellon, retail investors make up 25% of equities' total traded volume. In November, BlackRock opened the door for retail investors to vote in proxy battles through a UK pilot (Financial Times). When it comes to ESG, BlackRock’s actions are a fairly good leading indicator of what other large asset managers might do. This means that going into 2023, investor relations officers will need to be mindful of engaging with retail investors through social media and trading platforms.

For the Investor

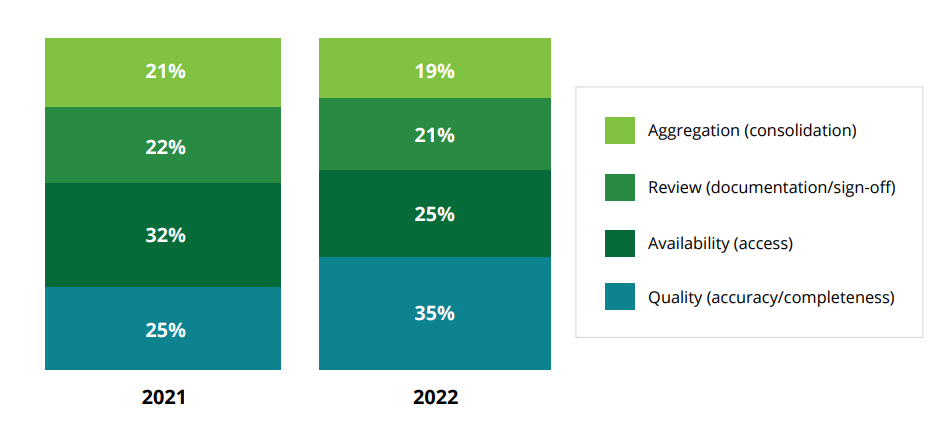

Prepare for mandated climate-related disclosures: The growing list of mandated disclosure for public companies will continue to lengthen. The regulatory environment continued to move at a rapid speed this year and we expect the proposed disclosure requirements to materialize in 2023. With the SEC's proposed proposal, companies will be required to include information about climate risks that are reasonably likely to have a material impact on their business, including operations, financial condition, and climate-related metrics included in registration statements and periodic reports. Companies will be mandated to report on climate-related governance, transition or scenario plans, risk management processes, and their direct greenhouse gas emissions including scopes 1 -3. One of the goals of the proposal was to make companies' disclosure more useful and more reliable for investors however we do not believe comparability and the consistency of the data is on the near-term horizon. This is because companies are still working towards understanding how to incorporate climate-related disclosures into their overall business strategy. While the SEC proposal has taken a stance that climate risks is investment risk, we believe companies will have to allocate significant resources to meet all the requirements of the proposal and have to heavily footnote how their emissions were calculated, especially scope 3. In a recent survey conducted by Deloitte of 300 executives from public companies, more than a third of executives stated that quality remains their greatest challenge with ESG, which surpasses last year's of just 25%.

Expect a global framework to materialize paving the way for more consistent disclosure: One of the challenges we expect investors to continue to face is the lack of consistency of ESG data being reported, though it is getting better. This year we saw a notable movement towards a global convergence amongst standards to attempt to create one dominant framework companies can align with. Last year at COP 26, the International Sustainability Standards Board (ISSB) was created to consolidate the Climate Disclosure Standards Board (CDSB) and the Value Reporting Foundation (VRF). Following this announcement, the GRIs standard-setting board, the Global Sustainability Standards Board (GSSB), and the IFRSF which is the standard-setting board for the ISSB announced a joint collaboration agreement to also work on alignment between the organizations. This is all to say, progress is being made for a global baseline that will help catalyze consistent data which can then be monitored, assured, and integrated effectively into company and investor decisions. This will be critical as companies are facing greenwashing pressures from investors and investors are facing greenwashing claims from regulators. A defined framework moving forward will help provide guidance on what to disclose, comparability between reporting periods, and ensure the information being reported is decision-useful. Moving into 2023, expect to see this global convergence

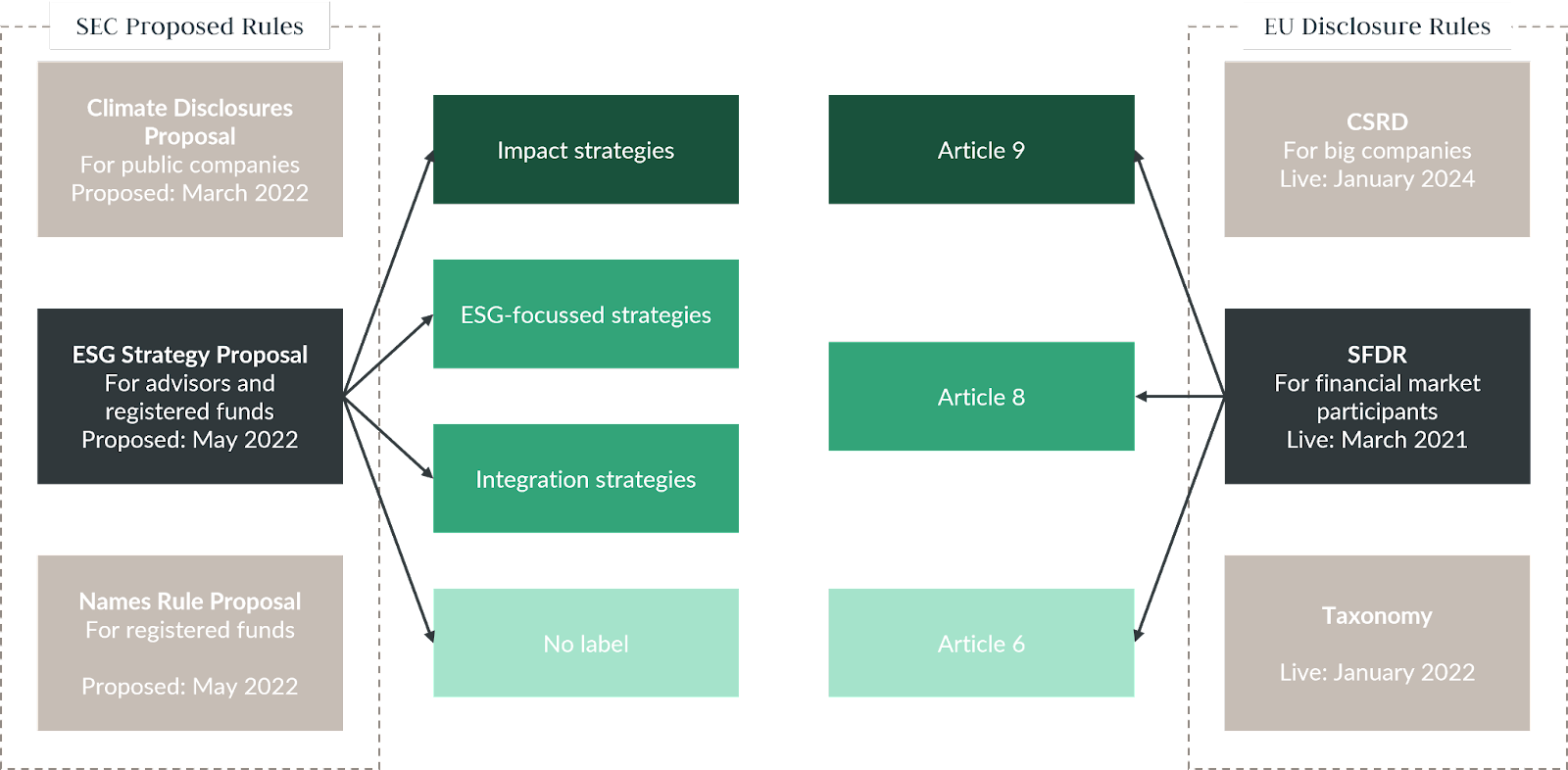

The SEC & EU FCA will continue to identify greenwashing, so prepare to back ESG-related claims with empirical data: Greenwashing increasingly became a regulatory concern through 2020. Greenwashing can happen at the firm, fund, or product level. Investors feel the pressure as society demands more sustainable products that align with their values. However, the mounting pressures to have competitive products could lead to overstatements of the fund or products deemed “sustainable”. This year we saw the SEC propose new rules for how investment advisors or funds market their ESG-related products.According to the SEC, it's been almost 20 years since the “Names Rule” was updated. This rule provides a framework for how funds are named and states at least 80% of the funds' assets must be invested in the type of focus stated in the name. The new legislation would expand the requirements to include further transparency on funds with growth, value, or ESG, for example. For ESG-related terms in the fund's name, this could include “socially responsible”, “ethical”, “green”, and “impact” [2]. In the EU, the Financial Conduct Authority (FCA) is tackling greenwashing through SFDR. SFDR has been in effect since 2021 but moving into 2023 the initiative will include a more detailed standard to supplement disclosure. Companies, firms, and asset managers should take steps to mitigate greenwashing by first disclosing the sustainability data to support ESG-related claims. This includes footnoting the limitations or scope of the data collected. For investors, clearly state the fund's objective, have investment policies and documentation to support, and have an ongoing evaluation process for ESG-related metrics.

Source: MJ Hudson

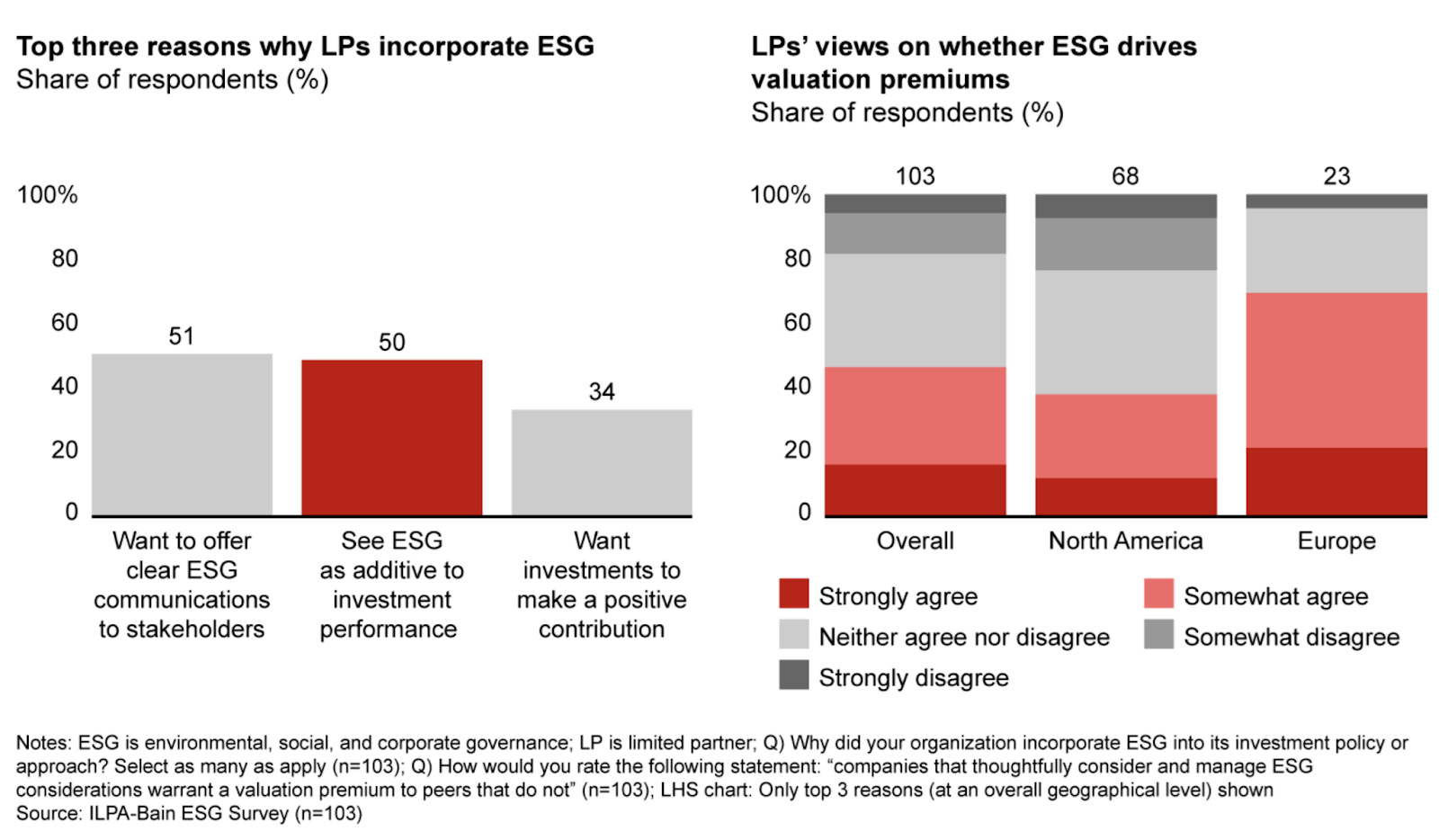

Develop a plan for engaging with LPs on ESG topics: No longer is ESG just relegated to publicly traded companies or asset managers. Limited partners (LPs) are embracing ESG integration at increasing rates. In February of this past year, a survey conducted by Bain & Company found that 70% of LPs include approach to ESG in their investment policy and 50% of LPs see ESG as additive to investment performance. Increasingly, we are seeing LPs engaging with asset managers on their responsible investing strategies and the ESG performance of their portfolios. We’ve seen frameworks emerge that are geared towards helping LPs evaluate the ESG integration of general partners (GPs), such as ILPA’s ESG Assessment Framework. Going into 2023, it is important for asset managers to prepare for inbound ESG questionnaires from their LPs and plan for more regular engagement on these topics.

Source: Bain & Company

For the Banker

Expect ESG to impact M&A: Over the last couple of years we’ve seen ESG influencing dealmaking and M&A press releases. ESG factors are increasingly becoming drivers in M&A activity through both value creation and risk mitigation. On the value creation side, a target’s ESG performance can increase its long-term value and send positive signals to investors. On the risk mitigation side, it is critical to assess the acquirer’s identified ESG issues and goals and the target’s alignment with them. Poor ESG performance can cause financial and/or reputational risk. To understand how ESG issues are influencing each step in the process going into 2023, we will be breaking them down below:

Before the deal: ESG factors may impact the willingness of potential acquirers and targets to interact. A potential acquirer may opt not to engage with a target company with weak ESG performance or misalignment with the acquirer’s ESG goals and policies.

Letter of intent and due diligence: ESG factors will influence the assessment and valuation of a target. In preparing due diligence materials, the first step is to examine whether ESG data exists and is accurate. Then, risks are identified, including physical and transition risks. Increasingly, acquirers are interested in whether the target’s current business practices will be regarded favourably by stakeholders such as investors and customers.

Negotiating the definitive agreement: While it is still rare in the U.S. for M&A agreements to include ESG clauses, we expect to see an emergence of ESG-specific clauses. These could potentially including specific representations and warranties, changes to Material Adverse Effect clauses, closing conditions, and ESG-specific indemnities.

Signing, announcing, and closing: Over the last year, we’ve seen ESG topics make their way into M&A announcements. As an example, the announcement for ConocoPhilips’ acquisition of Shell’s Permian assets included mentions of alignment with the company’s 2030 emissions intensity reduction target. Additionally, ESG issues are beginning to be factored into the 100-day or 12-month plan after the acquisition.

After the close: ESG considerations continue after the closing of the deal, through post-merger governance and integration. For example, the acquirer’s policies may require changes to the target’s governance structure. Additionally, ESG issues identified during the due diligence process may need to be addressed. For example, a poor safety track record may require changes to policies, risk management structure, and training programs. Integration efforts should focus on the ESG goals of the combined entity.

Plan for changing access to capital: Last year, Forbes published an article entitled “ESG is Banking’s Next Big Thing”. While we have seen changes in access to capital and banking over the course of the last year, 2023 is when we expect the rubber to really hit the road. Banking is a highly regulated industry, and as such its participants have long assessed and addressed governance issues. In recent years, they’ve increasingly focused on social issues in response to the Community Reinvestment Act. Now, banks are beginning to assess environmental factors as they begin to understand the impact of environmental considerations on risk within their lending and investment portfolios. In May, President Biden issued an executive order that directs the Financial Stability Oversight Council to find ways to assess climate-related financial risk. The Federal Reserve and the Office of the Comptroller of the Currency are also exploring ways to require banks to measure such risk, with a proposed framework being announced just earlier this month. On December 2nd, the Federal Reserve Board proposed a high-level framework for the “safe and sound management of exposures to climate-related financial risks for Board-supervised financial institutions” (Federal Register). This framework will apply to financial institutions with over $100 billion in total consolidated assets and the comment period ends 2/6/23.

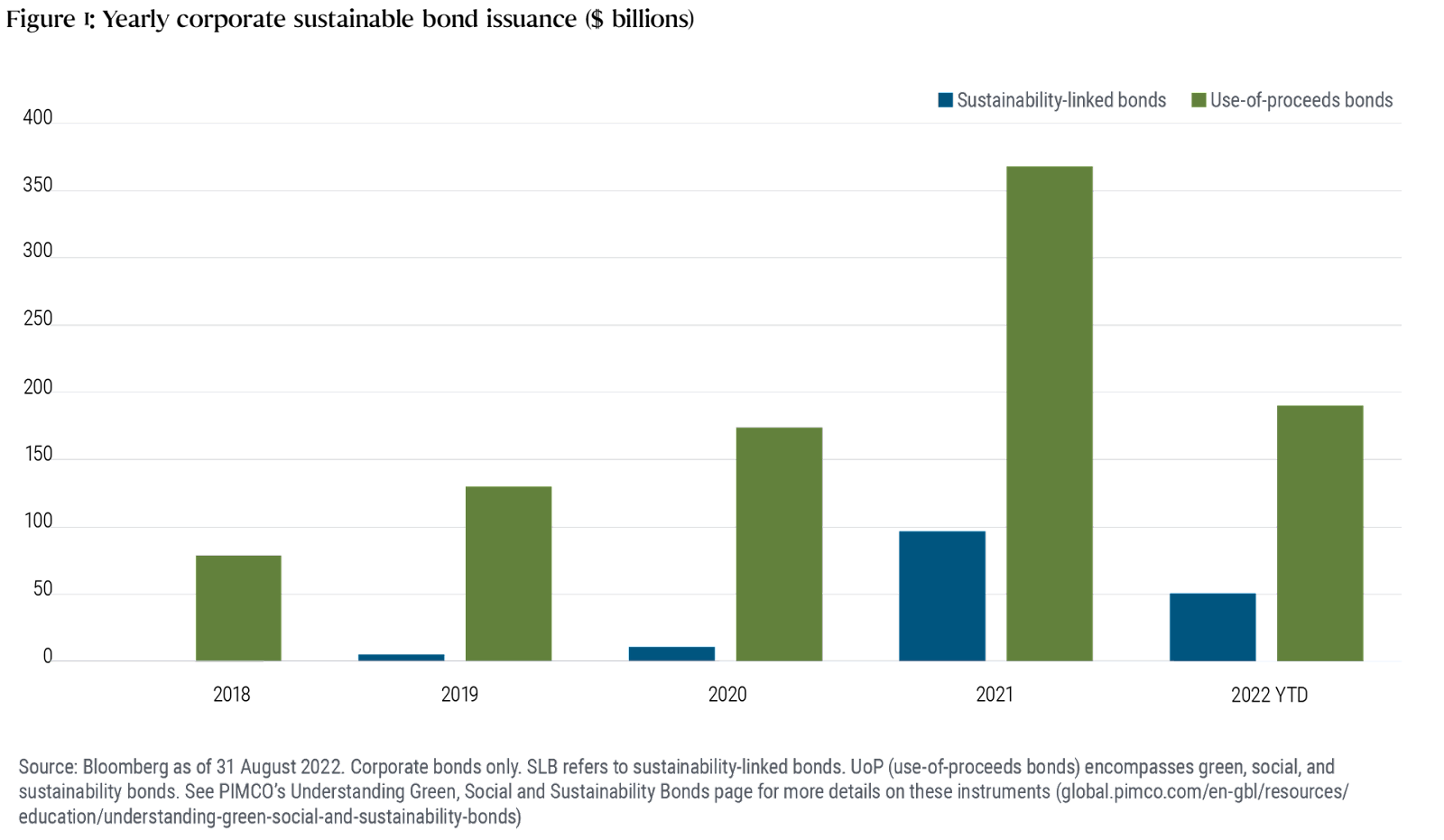

Watch out for the rise in sustainability-linked debt issuances: The sustainability-linked bond (SLB) market is one of the most rapidly growing segments of the capital markets, as investors increasingly seek to align with international sustainability goals. Last year, the total volume of SLB issuances exceeded $1T (according to Bloomberg New Energy Finance). It is important to understand the difference between SLBs and traditional green bonds. Where green bonds (and other social use-of-proceeds bonds) require funds to be dedicated to specific environmental or social projects, SLBs fund the operations of issuers that explicitly link sustainability objectives across their business with financing conditions. In practice, this would mean that if an issuer did not hit a particular emissions reduction target or produce health & safety KPIs below a certain threshold, the coupons would step up. Primary benefits include enabling issuers to access cheaper financing and allowing investors to diversify across geography, bond maturity, industry, or bond rating. These benefits, paired with tailwinds in consumer preferences for ESG investing, lead us to expect this trend of increasing SLB issuance to continue going into 2023. However, similar to issues related to greenwashing in the equity markets, we expect some challenges around accurate representation of ESG performance.

Source: Pimco

Understand the ways that ESG will continue to influence IPOs: For companies considering going public, it is important to understand listing requirements related for ESG. For example, NASDAQ requires at least two diverse board members (or disclosure of why this minimum was not met) as well as disclosure of board diversity statistics. It is also important to understand how ESG considerations have the potential to influence the overall success of the IPO. Investors in the public equities markets are getting more sophisticated in their evaluation of companies’ ESG performance, so the learning curve for companies who are preparing to go public can be quite steep. Going into 2023, we expect ESG to continue influencing the IPO process, including pre-IPO fundraising, “test the waters” meetings, and reception of the offering itself.

For the Intern / Student

The demand for sustainability professionals is growing across sectors. Students can pursue sustainability-related majors in fields like science, engineering, and design. These majors can prepare you for a variety of career paths, such as environmental law, environmental engineering, non-profit work, or ESG investment management. Individuals in these professions can act as stewards of natural resources by conducting research, identifying eco-friendly alternatives, and guiding investors, policymakers, and companies toward more sustainable decisions.

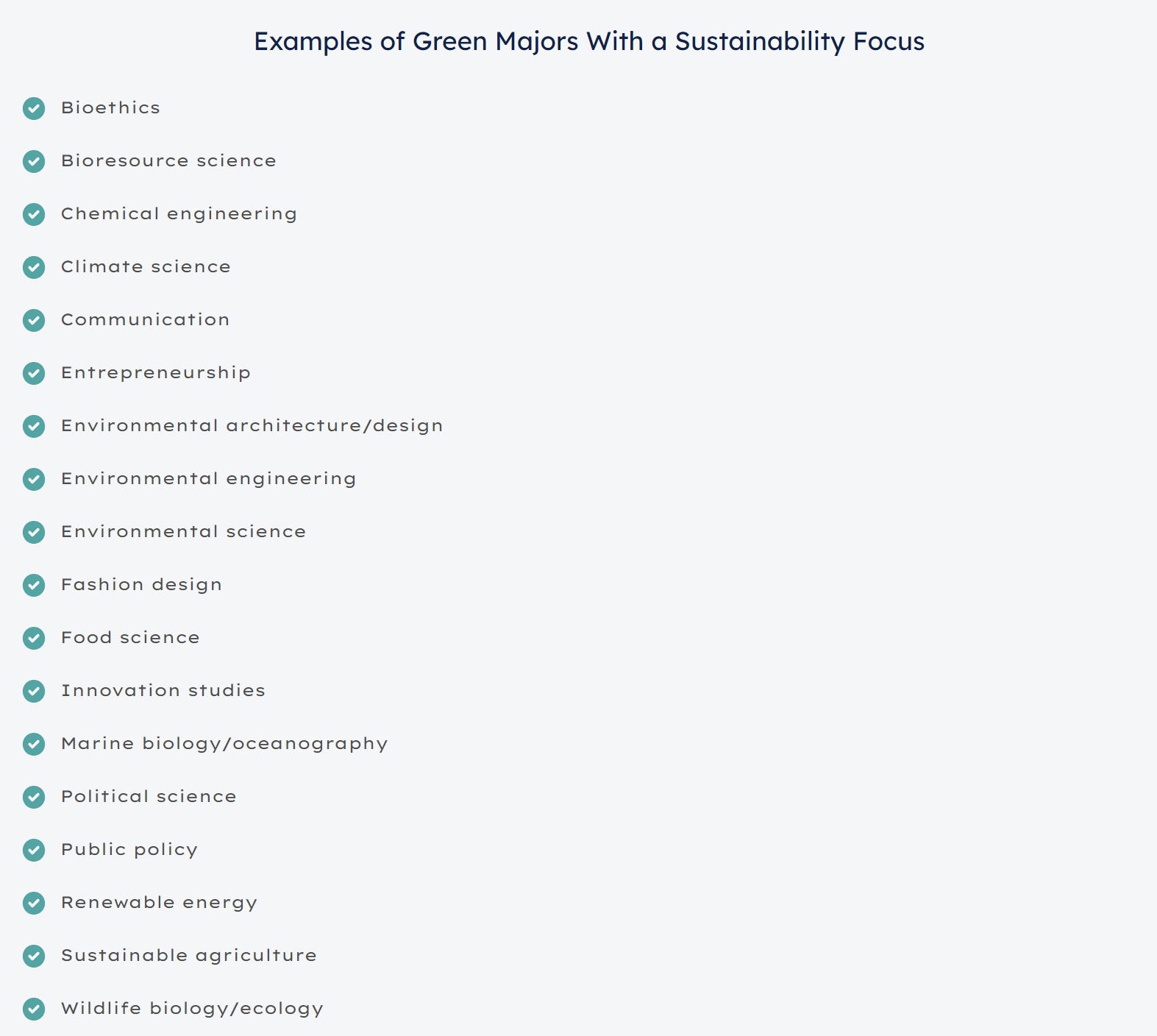

Build your foundation in school by choosing a related major: Degrees related to sustainability come in many forms. According to Best Colleges, some majors, such as environmental studies, innovation studies, and bioethics, focus specifically on sustainability, whereas others include sustainability in their curricula but take a wide-lens approach.

Source: Best Colleges

Work on your people skills and professionalism through informational interviews: The first step here is hitting up your family and friends to see if they know anyone in a sustainability-related field and asking for an introduction. Next, reach out to your career center. Most universities have career centers with career coaches who can make introductions to professionals either in their personal network or the school’s alumni network. Lastly, get comfortable with cold outreach on LinkedIn. One of the best ways to find people in professions you are interested in is through LinkedIn. Use keyword searches and look for people you have connections in common with or who might have gone to the same school, then draft a personalized message asking to connect.

Get involved - either through an internship, volunteer work, or student organizations: One of the best ways to try out a career (and build your resume) is by getting some practical experience either by interning, volunteering, or getting involved in student organizations.